I sip my black coffee in a dimly lit Palo Alto diner, staring at Legal Complex’s Q1 2026 report on my tablet, as the numbers mock the ‘booming’ narrative everyone’s peddling.

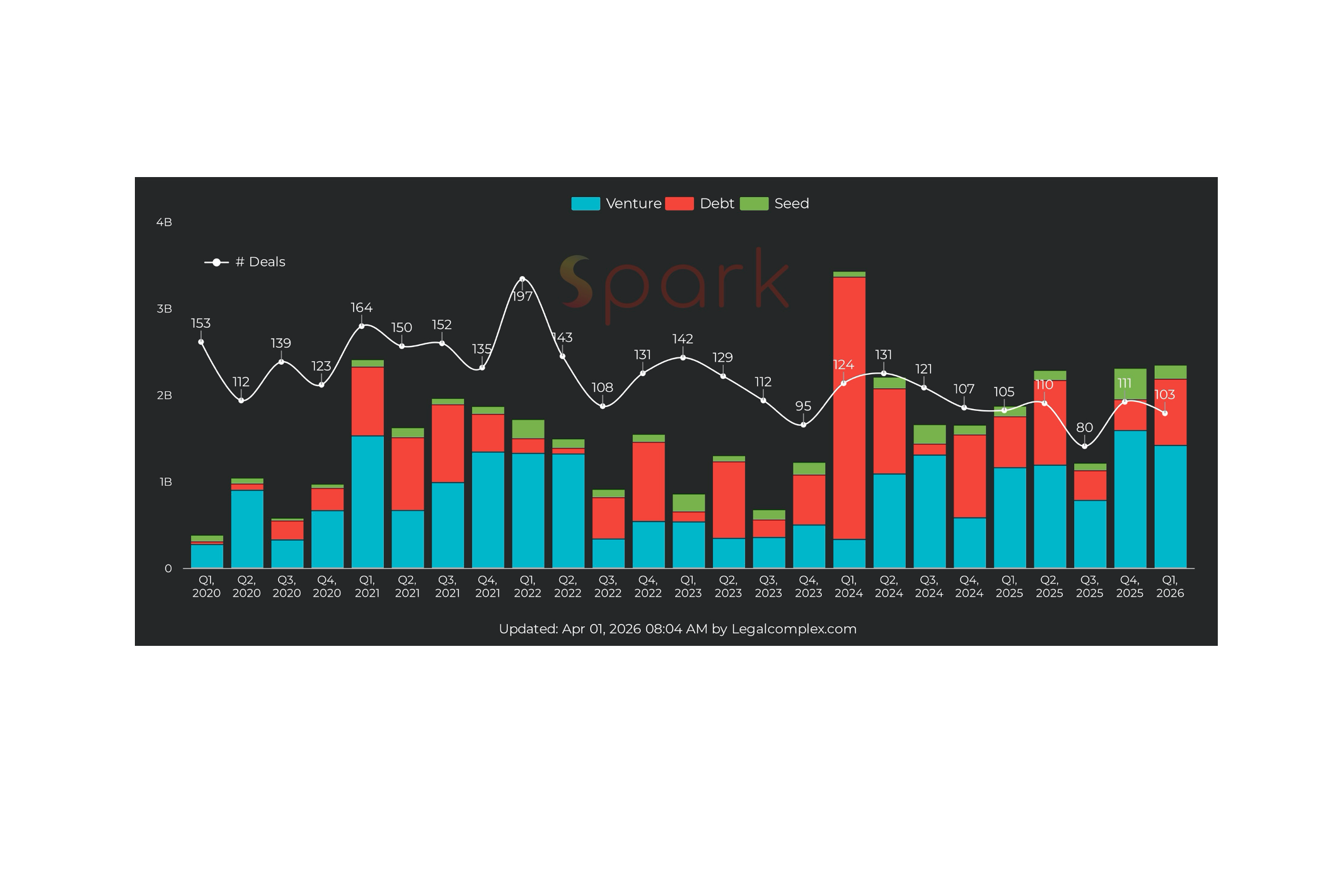

Legal tech funding hit $2.34 billion across 103 deals. Impressive, right? But here’s the kicker—Relativity, Harvey, and Legora sucked up 63% of it, a mix of equity and debt that leaves the rest scraping for crumbs.

Median round? A measly $1 million. Top-heavy doesn’t even cover it. You’ve got these giants feasting, then a long tail of dozens of minnows barely staying afloat. And look, Relativity’s $720 million debt facility—30% of the quarter’s total by itself—dwarfs everything, timed perfectly ahead of their whispered IPO dreams.

Why Are Harvey and Legora Printing Money?

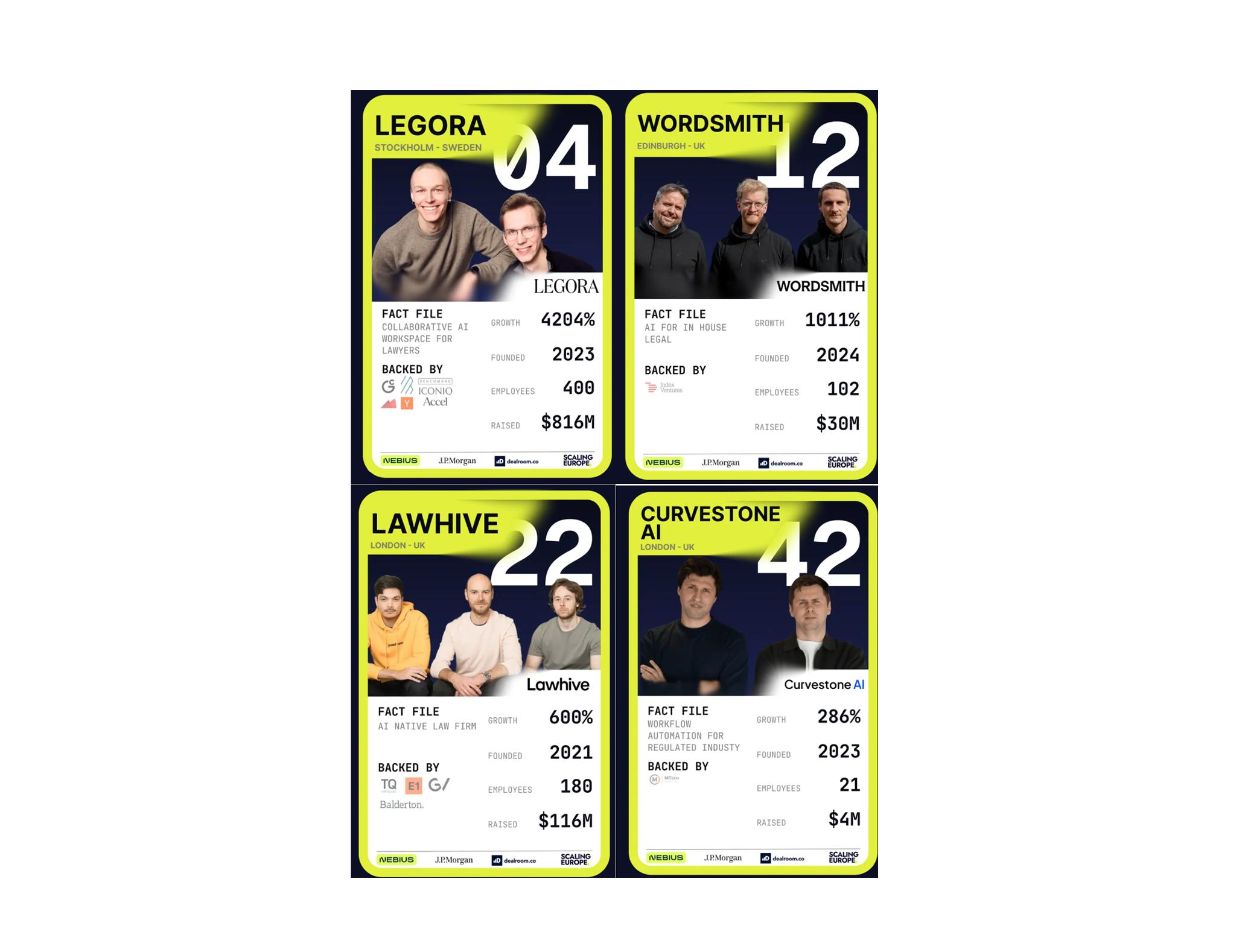

Legora’s $550 million Series D from Stockholm pushes their war chest to $816 million. Harvey? Another $200 million Series G, lifetime haul now $1.22 billion in three years. No other legal tech outfit’s hit a billion in VC like that. It’s Hargora (that’s Harvey + Legora for the uninitiated) dominating, with go-to-market machines that scare off competitors.

But who’s actually making money here? Not the lawyers upgrading their tech stacks overnight. These rounds scream ‘scale at all costs,’ Valley gospel from the 2010s that crashed hard. Remember WeWork? Or Uber burning billions before profitability flickered? History whispers: big funding often masks shaky unit economics.

“Harvey has now raised over a billion dollars in roughly three years of existence’ – and no other legal tech company has ever done this with VC funding.”

That’s from Legal Complex, and it’s the stat everyone’s quoting. Fine. But my unique take? This mirrors the dot-com bubble’s infrastructure plays—everyone chased the ‘platform’ dream, only for most to consolidate into AWS clones. Legal AI’s heading there: a Big Five (Relativity, Lexis, Harvey, Legora, Clio) lording over fragments.

Other rounds pepper the list—Fieldguide’s $75 million for GRC in San Francisco, Factify’s $73 million seed from Tel Aviv on documents, Lawhive’s $60 million legal services play in London. Crosby, Orbital Witness, Ivo, Summize—all hitting $50-60 million, heavy on contracts and ‘NewMods’ (new models for legal services, if you’re new).

Three of the top ten are reinventing legal delivery itself. Sign of the times? Or just VCs betting on disruption that law firms—stubborn, siloed—might ignore?

Is Seed Surge a Fresh Startup Wave or Dead End?

Raymond Blyd at Legal Complex drops gold: seed deals (46) topped growth rounds (44) for the first time since Q1 2024.

“That suggests a fresh wave of legal AI startups entering the market. The question is whether they’ll find their way to Series A or join the growing pool of companies that raised seed between 2023 and 2025 and haven’t raised since. That number was 979 when I last checked.”

Seeds surging feels bullish. But I’ve covered enough cycles to smell caution. That 979 zombie pool? It’s the graveyard of hype. Newbies flood in chasing Claude-for-Word dreams, but investors now fret big models commoditizing narrow tools like contract review. Why bet on a $10 million doc-AI when Anthropic does it free in Word?

And consolidation? Everyone’s talked it for years. Legal market’s too vast, fractured—firms pick boutique over best-in-class. Yet Hargora’s scale might force mergers. Smaller players get acquired or starve.

Here’s the thing.

Legal tech’s atomized chaos sustains dozens of overlaps. Huge. Complex. Law firms love their toys. But as Harvey and Legora stack billions, they’ll hoover talent, clients, data. The tail shrinks.

Prediction: by 2028, we’re down to 10-15 viable platforms, not 100. The rest? Features in the Big Five. VCs know it—that’s why they’re piling into leaders.

Claude for Word? Game-changer for valuations. Investors once drooled over contract AI ‘guaranteed growth.’ Now? Lawyers might stick to Microsoft, plug in Claude, done. No need for startup middlemen. Spin that as ‘ecosystem play,’ but it’s erosion.

Relativity’s debt? Smart chess. Funds expansion sans dilution, IPO bait. But debt bites if growth stalls. Seen it with SaaS darlings post-2022.

Who Wins in This Cash Flood?

Bottom line: money’s flowing because legal spend’s endless—$1 trillion global market. But winners are few. Hargora duo grows, draws more cash, crushes. Others innovate in niches or get eaten.

Skeptical vet says: don’t drink the ‘everyone thrives’ Kool-Aid. Follow the money. It’s pooling at the top, and gravity pulls harder each quarter.

🧬 Related Insights

- Read more: Stanford Dethrones Yale: Inside the U.S. News Law Rankings Earthquake

- Read more: Iran’s Internet Goes Dark for 12 Days: Access Now Slams Shutdown as War Rages

Frequently Asked Questions

What companies dominated Q1 2026 legal tech funding?

Relativity ($720M debt), Legora ($550M Series D), and Harvey ($200M Series G) took 63% of $2.34B total.

Is legal tech funding still booming in 2026?

Yes, $2.34B across 103 deals, but top-heavy with medians at $1M—seeds surging, growth lagging.

Will big legal AI firms consolidate the market?

Likely—heading to a Big Five dominance, with niches surviving but many seeds failing to scale.